This scenario covers entering a transaction in a subsidiary company with an accounting currency of USD and then consolidating to a consolidation company having EUR for accounting currency. In this scenario there is a balance sheet account that has been consolidated, followed by two currency revaluations to demonstrate the impact. (NOTE: The scenario can be reversed as well; the source company can be EUR with consolidation company using USD. )

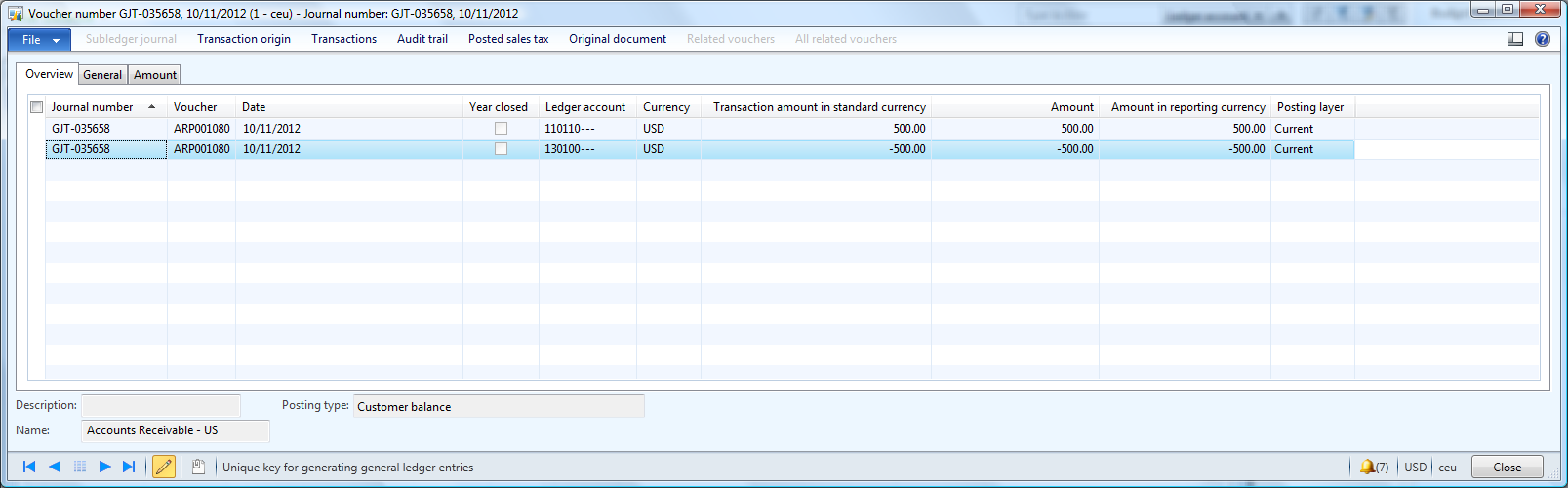

To start the scenario, I created a cash receipt in the subsidiary company CEU (source company). CEU operates in USD as the accounting currency. Below is the journal entry that was created for the cash receipt and we’ll work with this transaction through the consolidation process and subsequent foreign currency revaluations. The Cash receipt is dated 10/11/2012 for USD 500.00.

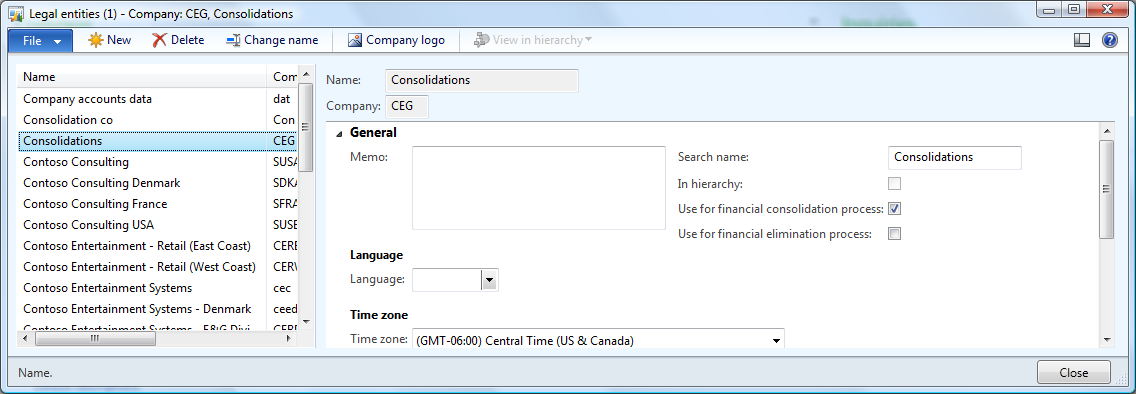

Now I switch focus to the consolidation company: CEG. (NOTE: This is a company I created for illustration purposes, and is not default in Contoso data) This legal entity is defined as a consolidation company by the field ‘Use for financial consolidations’ in the Legal entities form. (Organization administration | Setup | Organization | Legal entities.)

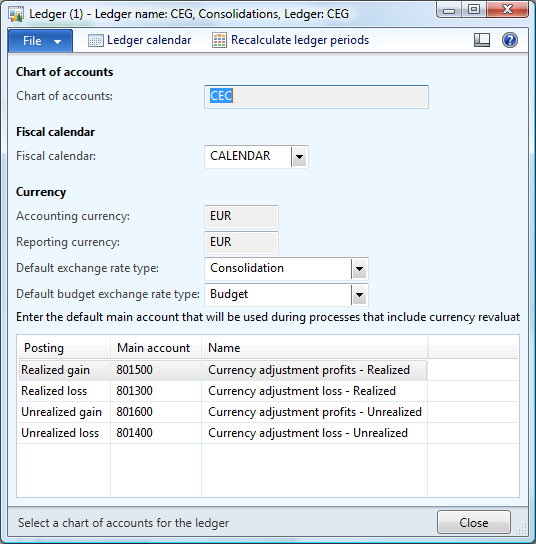

The following has been defined for the CEG legal entity’s Ledger:

– I am using a previously defined Chart of accounts (CEC), but a new COA may be defined for the consolidation company. (NOTE: Any accounts used in the consolidation process will be added to the chart of accounts for the consolidation company if not previously defined.)

– The accounting currency for the consolidation company is EUR.

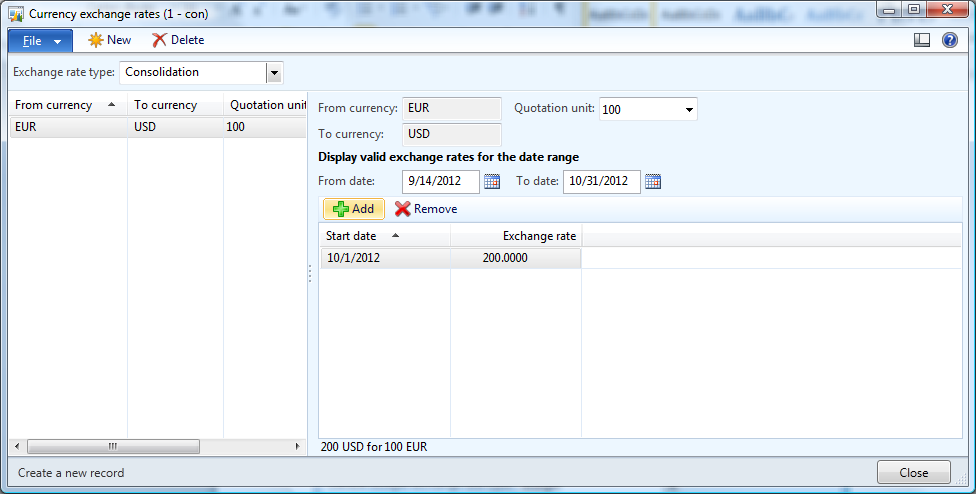

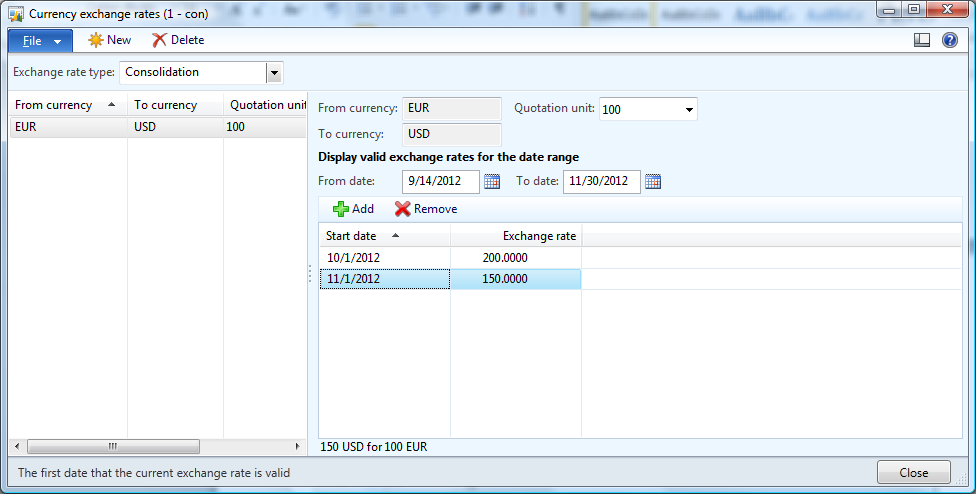

I created an exchange rate type called Consolidation to use for this company. The following exchange rate exists for the period starting 10/01/2012, which will be used for the exchange rate calculation during the consolidation process for the entry in CEU based on the transaction date of 10/11/2012. I am using an exchange rate of 200.00 for simplicity in explaining the calculations.

Now perform the Consolidation using the consolidation online process. (General ledger | Periodic | Consolidate | Consolidate (Online)) For illustration purposes, select the range of accounts that encompasses both the Cash and A/R accounts used on the original cash receipt journal from the subsidiary CEU company.

– Date range covers the date of the cash receipt entry.

– Marking ‘Rebuild balances during the posting process’ during consolidation will update the financial dimension sets used for reporting purposes in the consolidation company.

– I did not include financial dimensions in this illustration. However, you can use the financial dimensions tab to select the dimensions that you want to include in the consolidation process.

LEGAL ENTITY TAB:

I have selected the source company CEU for 100.00.

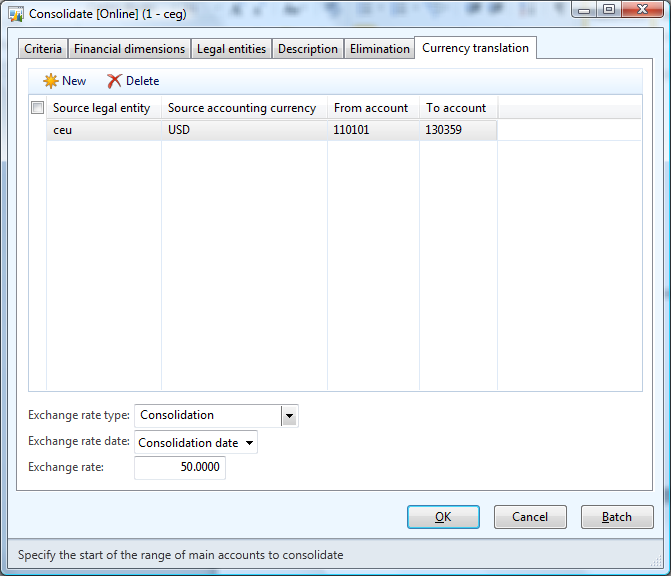

CURRENCY TRANSLATION TAB:

– Again I included a range of accounts that would cover the Cash and A/R accounts.

– Select the rate type to use for consolidations and you will see the exchange rate to be applied, which in this case is 50% based on the previously defined exchange rate of 200 USD = 100 EUR.

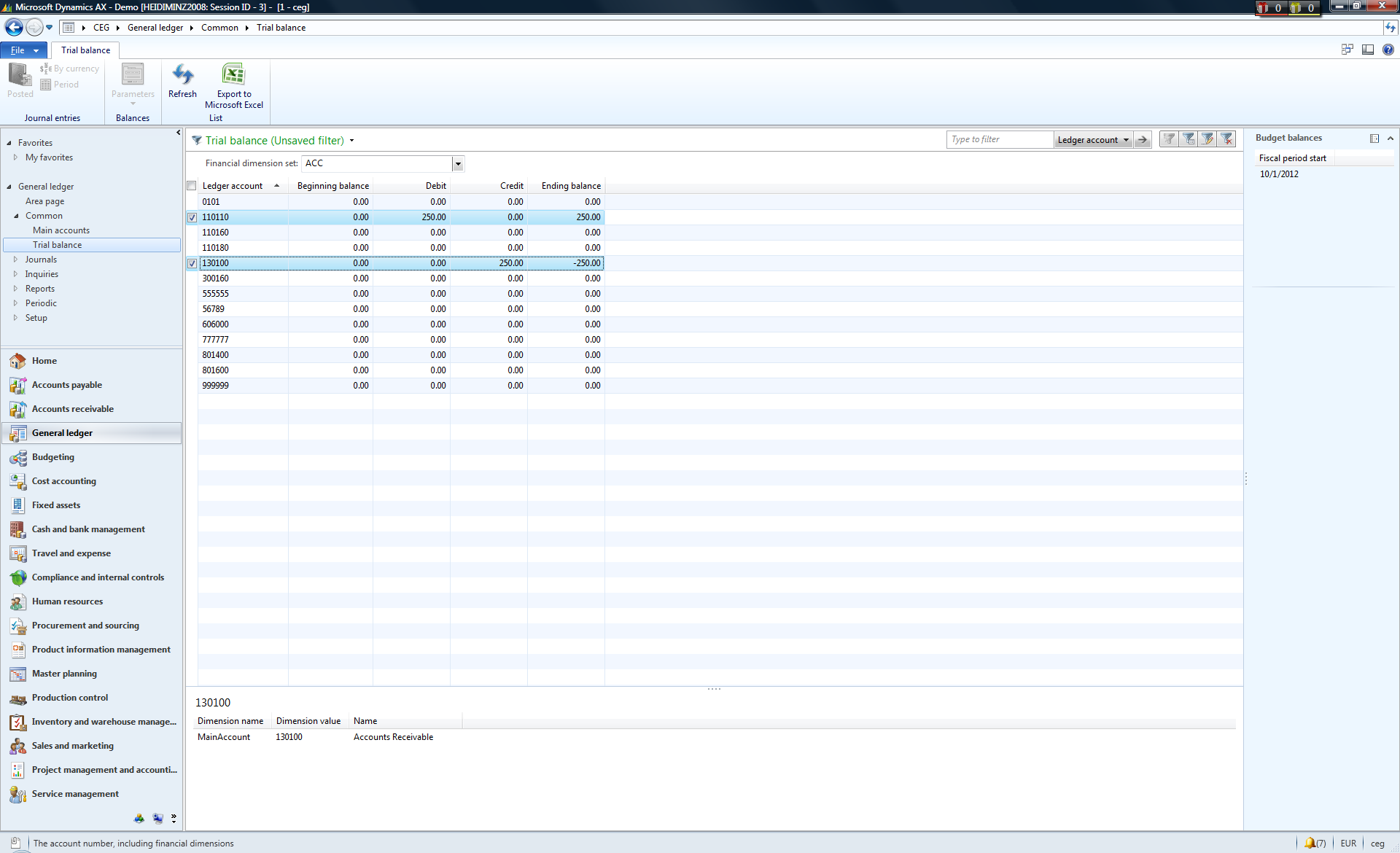

Select OK to perform the consolidation. Now navigate to the Trial Balance to see the balance for both the Cash and A/R accounts of 250 EUR, which is calculated as 500 USD * 50% = 250 EUR. (NOTE: Be sure to set the Date range for the Trial Balance list page in the Parameters action via the List page)

Now, update the currency exchange rate for the Consolidation exchange rate type (or whichever exchange rate type is being used by the Consolidation company’s Ledger). In this case, I have added a new exchange rate dated 11/01/2012 of 150.00

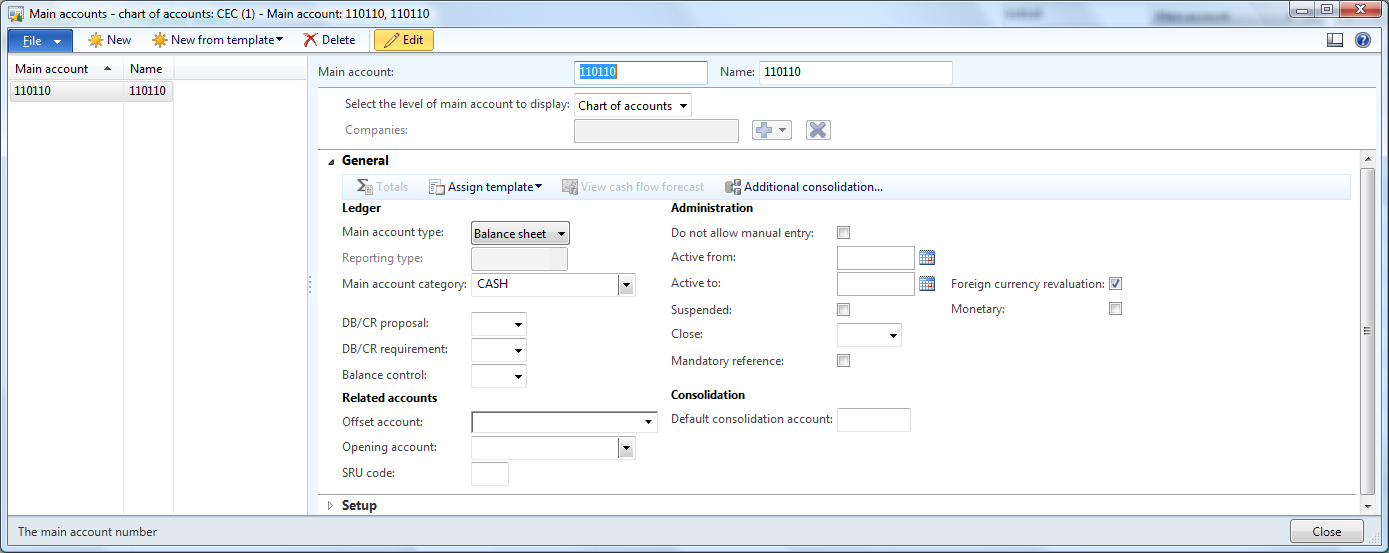

Next a foreign currency revaluation will be performed in the Consolidation company. However, first, ensure that the accounts that you want revalued have the ‘Foreign currency revaluation’ option marked in the Main accounts form.

Perform a foreign currency revaluation in the Consolidation company (General Ledger | Periodic | Foreign currency revaluation) using the following criteria:

Next you can view the results of the entries that were posted for the adjustment of exchange rate from 200.00 to 150.00. The amount is calculated as follows:

– Original transaction amount in USD: 500.00

– The exchange rate in use for 10/01/2012 through 10/31/2012 = 100/200 or 50%

– Original amount posted during consolidation = 250 EUR (500 * 50%)

– Revalued amount:

* Original transaction amount: 500

* The exchange rate in use for foreign currency revaluation 11/01/2012 through 11/30/2012 = 100/150 or 66.6667%

* 500 * 66.6667% = 333.33 EUR

* The new balance for the cash account is 333.33 EUR and the amount that is posted as exchange adjustment is the delta betwen the original EUR amount and the revalued amount: (250.00 – 333.33) = 83.33 that is posted.

Here is the balance on the Trial Balance list page after the foreign currency revaluation:

And the journal entry that was created. Please note that there are duplicate entries for each account due to the adjustment for the reporting currency as well as the accounting currency. (NOTE: In this example, the accounting currency and the reporting currency are both EUR, but the reporting currency could be different than EUR, as necessary)

Now modify the exchange rate again for 12/01/2012. I updated the exchange rate to be 100.00. As a result of this, after the foreign currency revaluation, the balance of the cash account should be 500.00 = to the original amount of the transaction in USD.

And I then perform the foreign currency revaluation in the consolidation company again using the following criteria:

When you view the Trial Balance list page, you can see that the amounts have been adjusted to 500.00 and the appropriate gain/loss is recorded.

When you view the entries that were created, they reflect just the difference in exchange rates. Again, two entries were created: one for the accounting currency; and the other for the reporting currency. (NOTE: In this example, the accounting currency and the reporting currency are both EUR, but the reporting currency could be different than EUR, as necessary)

500 * .6667% = 333.33 (from prior revaluation). 500 * 100% = 500. (333.33 – 500.00) = 166.67 that is posted.

So this demonstrates that the foreign currency revaluation in the consolidation company does not completely reverse and treat the entire amount as an exchange adjustment if these appropriate steps are followed.